Buyers in the Tri-City purchase smaller flats, but more often for cash

A significant increase in housing prices in the Tri-City has caused buyers to shift towards purchasing smaller flats.

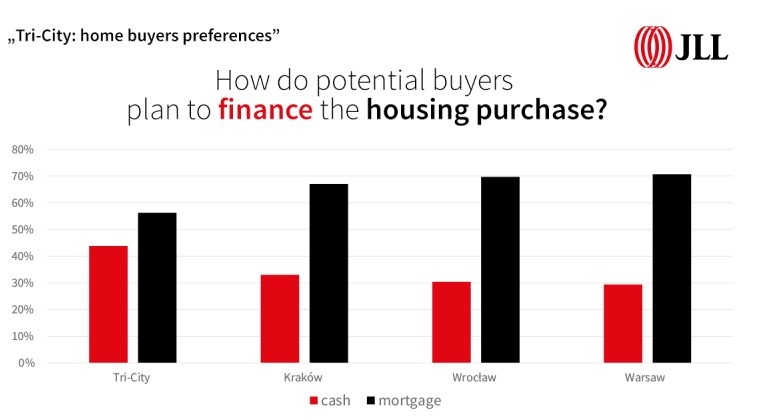

At the end of September 2019, the most sought-after units on the Tri-City market were one-bedroom units with an area of at least 36 sq m. The most numerous buyers, up to 30%, were couple1 willing to spend on average up to PLN 454,000 to buy a flat. Interestingly, in the Tri-City, buyers purchase housing for cash more often than in other cities, as many as 44%, according to the latest JLL report “Tri-City: home buyers' preferences”.

The Tri-City is currently the fourth largest housing market in Poland, with approximately 8,500 units sold per year. In terms of average housing prices, it is second only to Warsaw. Over the past three years, the average asking price for flats on offer has increased from PLN 6,800/ sq m to PLN 9,400/sq m, i.e. by 38%.

“In addition to high demand, the main factors responsible for this increase were the growing construction costs observed throughout the country and a significant increase from 21% to 43% of the share of upper-middle segment units and apartments in the combined offer of Gdańsk, Gdynia and Sopot since the end of 2017. Sales numbers, although slightly weaker than in previous years, still seem to be satisfactory for developers, which results from rising prices compensating for slower sales pace. This is undoubtedly thanks to investors who purchase units for rent”, says Aleksandra Gałabuda, consultant in the Housing Market Research Department at JLL.

Investment purchases drive the market

The JLL survey of the preferences of buyers who at the end of September 2019 were actively looking for housing on the obido.pl website, showed that the share of investors, i.e. buyers who purchase with a view to rent, was significantly higher in the Tri-City (20%) than in Warsaw (11%) or Kraków and Wrocław (15% each).

Investors in the Tri-City were primarily interested in one-bedroom units. Nearly 60% of respondents were looking for this type of unit. Studios were in much less demand. Only 8% of buyers were looking for units with an area of less than 30 sq m. For comparison, in the other three cities, as many as 17-20% of buyers purchasing units for rent were interested in this size. Tri-City investors were also not interested in units with more than two bedrooms, with only up to 1% of buyers looking for these types of units, while in other cities it was about 3-4%.

“The Tri-City rental market is quite specific due to the city’s tourist attractions. In addition to the regular groups ensuring stable demand for long-term rental, such as students or young professionals employed in the BPO and IT sectors, there is also a high and continuously growing demand for short-term rentals from tourists. In this group, apart from renting units for city breaks, which also generate demand in other major cities, there is also demand for rentals for longer holiday stays, especially in the summer. This determines the demand for a specific type of housing”, says Aleksandra Gałabuda, an expert at JLL Polska.

Cash purchases are more popular

As is the case in other cities, families in the Tri-City spend more money than other groups on housing. This is mainly due to their demand for larger premises. The average purchasing budget for this group is PLN 576,000. The budget of couples is 20% less, amounting to PLN 454,000. Singles, competing with investors for the same size units, spend around PLN 354,000.

Interestingly, in all three groups, buyers intend to finance the purchases from their own funds much more often than in other cities. Over 46% of couples looking for housing in the Tri-City purchase them with own funds, while in Warsaw, Kraków and Wrocław no more than 30% of buyers in this group intend to purchase for cash.

For more on the expectations of buyers on the Tri-City housing market and the other three largest housing markets in Poland, read the latest JLL report “Tri-City: house buyers' preferences”.

1The JLL assessment of buyer preferences was based on a survey conducted among OBIDO users who belong to one of the four basic groups: singles, couples, families and investors looking for units to rent