More offices and residential units in Katowice

The Katowice market sets records with 160,000 sqm under construction, 14% of the office space being built in the country, as well as over 1,400 new units launched for sale on the primary residential market.

In H1 2021, construction activity in Katowice was one of the highest in Poland’s regional cities. With 160,000 sqm, the Katowice office market accounted for 21% of new supply outside of Warsaw (14% nationwide) and with demand 47% higher y-o-y. The residential market was not idle either. 1,400 units were put up for sale in developers’ projects, and although the average price of new flats was 50% higher than just five years ago, sales in Katowice still set a new record for the first half of a year, according to data from the advisory firm JLL.

One of the most important elements driving growth in the office market is the business services sector (BSS). In the first quarter of 2021 the industry employed 355,300 people in Poland, 13,500 (3.9%) more than in the same period last year [1], with Katowice and the Upper Silesian and Zagłębie Metropolis (GZM) being two key locations.

According to ABSL data, Katowice and GMZ are among the five largest locations for BSS investments. The two locations play host to 115 BPO / SSC / IT / R&D centres, seven of which were opened in the last two years. At the beginning of this year, employment in the sector was 27,500, and the relative resilience of the industry to the turbulence caused by the pandemic means that the number of employees may exceed 28,900 by the end of Q1 2022. Of key significance for the potential development of this market is the offer of modern office space, which has been developing in the region over recent years.

Demand on the Silesian office market

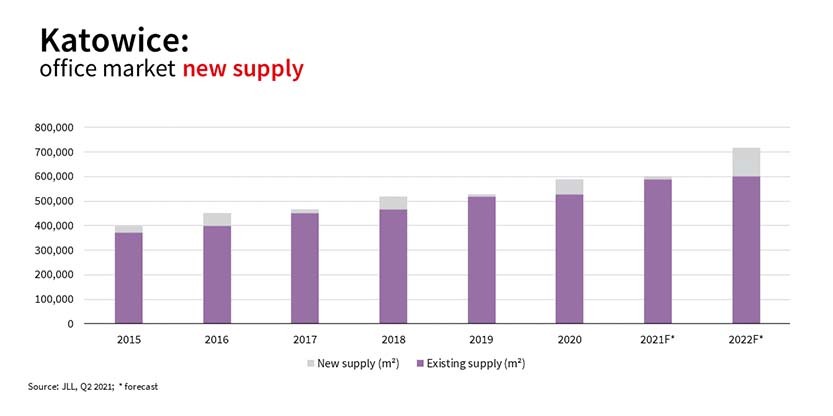

At the end of H1 2021. Katowice offered 591,000 sqm, making it Poland’s sixth largest market for office stock. The capital of the Silesian Voivodeship is also responsible for 15% of office demand outside Warsaw.

2019 saw record demand for offices in Katowice, when nearly 85,000 sqm was leased. Although leases signed in 2020 dropped 24% (65,000 sqm), it should be remembered that it was a not very favourable year for the office market.

”In the first six months of 2021, over 39,000 sqm was leased in Katowice. Nearly half of these were contract renegotiations. Uncertainty in the market and the fact that many tenants are in the process of developing new workplace strategies are currently holding back key leasing decisions”, comments Dorota Gruchała, Head of Kraków Office, JLL.

In H1 2021, the five largest leases in Katowice were the renegotiation and expansion of Rockwell Automation for a total of 19,500 sqm in A4 Business Park II, 4,300 sqm leased by UPC, 2,600 sqm signed by Hyland in the Global Office Park office building, the expansion of Keywords Studios for 1,900 sqm in the Green Park complex and 1,100 sqm leased by ista in Supersam.

Office developers continue to be active with 160,000 sqm under construction

760,000 sqm is under construction in the eight major office regional markets, with Katowice accounting for 21%. In 2020, 61,300 sqm was completed in this market, with a further 1,500 sqm was delivered in the first six months of 2021.

“From 2020 to the end of June 2021, five new office buildings with a total of approx. 62,800 sqm were delivered to the market. A further approx. 160,000 sqm is currently under construction, the second highest among regional markets. However, it is worth noting that the vast majority of this volume will be delivered to the market in 2022. As a result, Katowice will be seeing a record increase in supply. By the end of this year, approx. 10,000 sqm will have been delivered, which in turn may contribute to a slight increase in vacancy rates”, explains Ewa Grudzień, Senior Research Analyst, JLL.

The vacancy rate at the end of the first half of 2021 was 9.2%. The largest developments currently under construction total around 122,000 sqm and include Global Office Park (55,000 sqm, Cavatina), KTW II (40,000 sqm, TDJ Estate) and Craft (27,000 sqm, Ghelamco.

”It is possible that some of the investments planned for 2022 will be put back to 2023. This will depend to a large extent on what impact the pandemic and return-to-office strategies will have on the market in H2 2021 and H1 2022”, comments Dorota Gruchała, an expert at JLL.

Record sales on the residential market

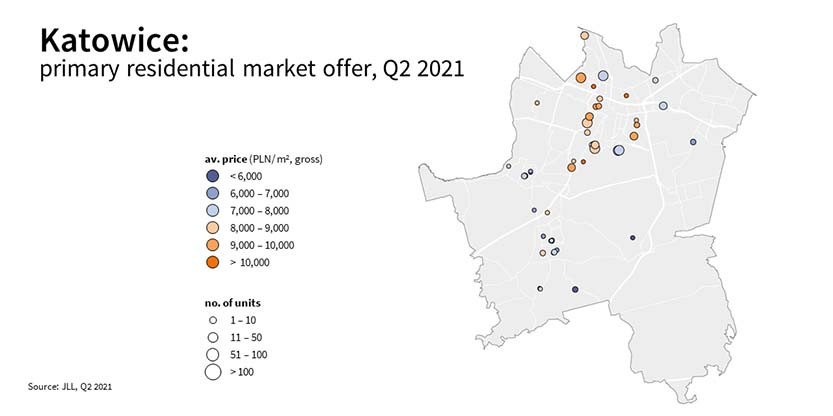

It is difficult to analyse the real estate market in Katowice without taking into account the agglomeration itself. Within the Silesian agglomeration there are several important urban centres which together represent the most populous area in the country. Katowice is the centre of the region and at the same time a location with most new residential investments. According to JLL, almost half of developer activity within the whole agglomeration is concentrated in Katowice. While in the Silesian Agglomeration about 5,000 new units were available for sale at the end of June this year, people looking to buy a flat in Katowice could choose from a pool of 2,000 units. Although Katowice has seen people from the city to smaller centres in the agglomeration and beyond, the market for new apartments has been steadily growing in recent years.

Sales of new units in Katowice, both in Q1 and Q2 2021, were close to the quarterly average of 2019’s record breaking performance. In fact, the over 600 units for each quarter meant that the market set a new H1 sales record.

New supply encourages buyers

“The return to high sales figures was made possible by significantly higher introductions. In other large markets, sales are increasingly dependent on supply. However, in the case of Katowice, buyers still have a choice. It should also be remembered that Katowice is slightly behind the main six cities in the market cycle. While in most of the largest markets (Warsaw, Kraków, Wrocław and Tri-City) the sales peak took place in 2017, in Katowice the best sales result - 2,500 units - was recorded in 2019. The arrival of the COVID-19 pandemic in 2020 clearly disrupted the rising volumes of both new launches and sales”, comments Katarzyna Kamińska, Manager, Residential Research, JLL.

The number of flats launched for sale in the first half of 2021 exceeded 1,400 and was one of the highest in recent years. This meant that the offer from developers operating in Katowice at the end of June 2021 included approximately 2,000 units. Although this result was 18% lower than the year before, in contrast to Poland’s largest markets, it did represent an increase quarter-on-quarter.

"The high level of interest in purchasing flats can be seen in all large markets. However, in Katowice demand has still not exceeded supply to the same degree as in other locations. What’s more, the results of the first six months of this year even indicate a slight surplus of new flats coming onto the market”, comments Katarzyna Kamińska, an expert at JLL.

According to JLL experts, competition for the primary market comes from the local secondary market. In this area, a large supply of relatively inexpensive flats on Katowice’s secondary market can be observed, especially in neighbouring cities such as Chorzów and Bytom. A certain group of buyers also prefers to live in newly built or renovated detached houses outside the city or in the greener suburbs.

Katowice apartment prices narrowing the gap with larger markets

Average prices of residential units in Katowice have been rising steadily every quarter since the beginning of 2018. All large markets behave similarly in terms of price growth and Katowice is no different. For a long time, until the end of 2017, prices in Katowice were stable with the average price per square metre for a residential unit being PLN 5,200. However, by the end of June 2021, the average offer price for units on the primary market was just under 8,300 PLN/sqm. This means an increase of almost 50% within just three-and-a-half years. Among the largest markets, only Kraków (55%) saw a larger increase in the average offer price during this period.

"Focusing on the recent quarters, it is worth emphasizing that the prices of flats in Katowice grew in line with those in other major agglomerations - by 5% q-o-q and by 11% y-o-y. Although the price of over 8,000 PLN/sqm in Katowice is at an all-time high and comes close to the price level we currently have on the market in Poznań, the exceptionally high sales recorded in recent months show that buyers are still able to accept these purchase prices”, explains Katarzyna Kamińska, an expert of JLL responsible for residential market monitoring.

----------------------------

[1] ABSL, Business Services Sector in Poland 2021